Modeling and simulation of the operational risk of fiduciary institutions in Colombia

Article Sidebar

Main Article Content

Abstract

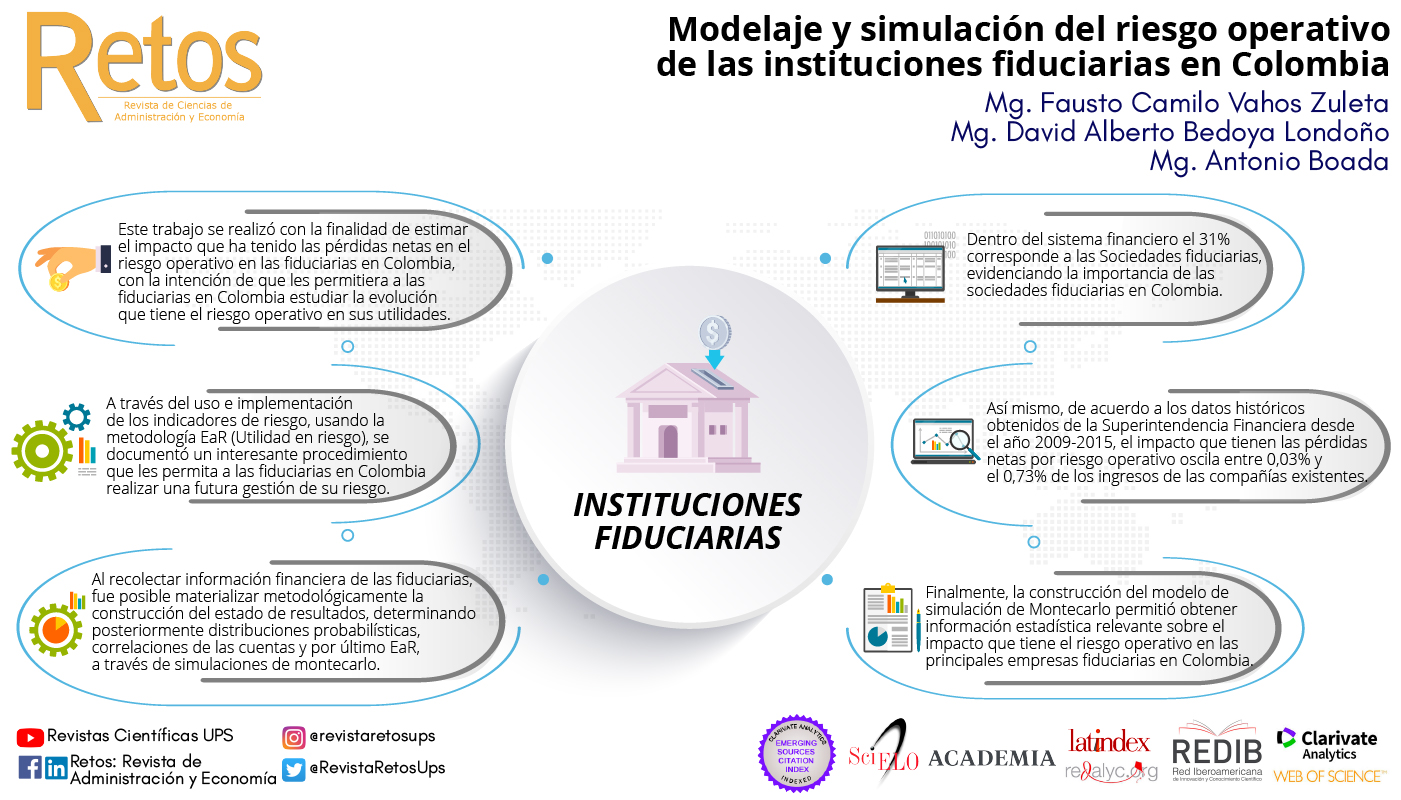

Through this work, a model was developed that has become the first experience to measure and forecast the impact that net losses have had on operating risk in fiduciary companies in Colombia and that would allow fiduciary companies to study and analyze the evolution and impact that operating risk has on their profits. The financial services industry sector has been exposed to a number of risks that lead to losses in these entities, and in the financial system in general; thus, through the definition of operational risk and operational risk management, the study of risk indicators is implemented through the EaR (Risk Usability) methodology, established in three phases: on the one hand, the selection and compilation of the financial information of the fiduciaries to be studied; the determination of the financial statements, with the construction of the income statement, and ending with the determination of the probabilistic distribution that adapts to the historical information, to then determine the correlations between the determined accounts, in order to be able to establish the EaR through Monte Carlo simulations. In this way, it was possible not only to build a model to quantify operating risk, based on financial information on income and expenses, but also to obtain relevant statistical information on the impact of operating risk.

Article Details

Authorship: The list of authors signing must include only those people who have contributed intellectually to the development of the work. Collaboration in the collection of data is not, by itself, a sufficient criterion of authorship. "Retos" declines any responsibility for possible conflicts arising from the authorship of the works that are published.

Copyright: The Salesian Polytechnic University preserves the copyrights of the published articles, and favors and allows their reuse under the Creative Commons Attribution-NonCommercial-ShareAlike 3.0 Ecuador license. They may be copied, used, disseminated, transmitted and publicly displayed, provided that: i) the authorship and the original source of their publication (journal, editorial and work URL) are cited; (Ii) are not used for commercial purposes; Iii) mention the existence and specifications of this license.

References

Antoine Frachot, O. M. (2003). Loss Distribution Approach in Practicee. Paris: Groupe de Recherche Opérationnelle, Crédit Lyonnais.

Asociación de Fiduciarias de Colombia. (enero de 2013). Asociación de Fiduciarias de Colombia. Obtenido de Asociación de Fiduciarias de Colombia: http://fliphtml5.com/kovh/madm

Basilea, C. d. (2004). Basilea II. Basilea: Press & Communications.

Carvajal, J. A. (2004). Guía para el análisis crítico de publicaciones científicas. Chil Obstet Ginecol, 69(1), 67-72.

Colombia, S. F. (22 de Diciembre de 2006). Circular Externa 048. Obtenido de www.superfinanciera.gov.co/NormativaFinanciera/Archivos/cc48_09.doc.

Cook, J. D. (24 de Noviembre de 2009). A beta-like distribution. (John D. Cook) Recuperado el 23 de 08 de 2017, de https://www.johndcook.com/blog/2009/11/24/kumaraswamy-distribution/

Cruz, M. (Enero de 2002). Modeling, measuring and hedging operational risk. John wiley and Sons, 346.

Draft International Standard ISO/DIS 31000. (s.f.). Risk management-principles and standardization. Obtenido de www.iso.org/ISO/home/standards/ISO 31000.htm

Fengge Yao, H. W. (2013). CVaR measurement and operational risk management in commercial backs occording to the peak value method of extreme value theory. Mathematical and Computer Modelling, 58, 15-27.

Griselda Dávida Aragón, F. O. (3 de Enero de 2015). Cálculo del valor en riesgo operacional mediante redes bayesianas para una empresa financiera. Contaduria y Administración(61), 176-201.

Holder Bonin, T. D. (2007). Cross-sectional earnings risk and occupational sorting: The role of risk attitudes. Labour Economics, 14(6), 926-937.

Jinmian HAN, W. J. (2015). POT model for operational risk: Experience with the analysis of the data collected from Chinese commercial banks. China Economic Review(36), 325-340.

José Francisco Martínez Sánchez, F. V. (2013). Riesgo Operacional en el proceso de pago del Procampo. Un enfoque bayesiano. Contaduria y Administración, 58(2), 221-259.

José Francisco Martínez Sánchez, M. T.-P.-M. (2016). An analysis on operational risk in international banking: A Bayesian approach (2007-2011). Estudios Gerenciales, 32, 208-220.

Juan Guillermo Murillo, M. A. (2014). Comité de Basilea. En Riesgo Operativo: Técnicas de modelación cuantitativa (pág. 13). Medellin: Sello editorial.

Linda Allen, T. G. (2007). Cyclicality in catastrophic and operational risk measurements. Journal of Banking and Finance, 31(4), 1191-1235.

Londoño, D. A. (2009). Propuesta para la modelación del riesgo operativo en una entidad financiera. Medellin.

Luz Mercedes Pinto Gaviria, A. L. (2008). Administración del riesgo operacional en Colombia. Estado de la implementación del SARO en el sector bancario. AD-minister, enero-junio(12), 89-106.

Mun., J. (2016). Modelación de Riesgos. En Modelación de Riesgos (págs. 160-161). New Jersey: Thompson-Shore and ROV Press.

Norma técnica Colombiana NTC 5254 2004-05-31. (s.f.). Gestión del riesgo. Editada por el instituto colombiano de normas técnicas y certificación (ICONTEC). Obtenido de http://www.corponor.gov.co/NORMATIVIDAD/NORMA%20TECNICA/Norma%20T%E9cnica%20NTC%205254.pdf

Palisade Corporation. (2016). Guia para el uso de @Risk. New York: Palisade Corporation.

Paul Embrechts, G. P. (2006). Aggregating Risk Capital, with an Application to Operational Risk. The Geneva Risk and Insurance Review, 31(2), 71-90.

Pavel V. Shevchenko, M. V. (2006). The Structural Modelling of Operational Risk via Bayesian inference: Combining Loss Data with Expert Opinions. The Journal of Operational Risk, 1(3), 3-26.

Periodico El Tiempo. (04 de Mayo de 2011). Más de 14 años de prisión a coautora de desfalco de Fidubogotá. El Tiempo.

Risk, A. B. (2010). V. Aquaro, M. Bardoscia, R. Bellotti, A Consiglio, F De Carlo, G Ferri. Physica , 389(A), 1721-1728.

Santiago Medina Hurtado, J. A. (2013). Estimación de la utilidad en riesgo de una empresa de transmisión de energía eléctrica considerando variables económicas. Cuadernos de economía, 32(59), 103-137.

Superintendencia Financiera de Colombia. (2006). Carta circular 049 de 2006. Obtenido de www.superfinanciera.gov.co/NormativaFinanciera/Archivos/cc49_06.rtf.

Superintendencia Financiera de Colombia. (Junio de 2007). Circular Externa 041 de2007. Recuperado el 23 de 0ctubre de 2016, de https://www.superfinanciera.gov.co/jsp/index.jsf

Superintendencia Financiera de Colombia. (2012). Circular externa 100 de 1995. Obtenido de www.superfinanciera.gov.co/normativa/.../cir100.htm.

The commitee of Sponsoring organizations of the treadway commission. (2005). Administración de riesgos corporativos-Marco integrado.

Valencia, A. M. (2009). Cuantificar el risgo operativo en entidades financieras en Colombia. Borradores de Administración, 25, 1-30.

Valencia, A. M. (2011). Riesgo Operativo I: Una revisión de la literatura. Borradores de administración, 2-32.

Valencia, A. M. (2011). Riesgo Operativo II: una revisión de literatura-Continuación. Borrador de Administración, 54, 1-20.

Valencia, A. M. (2013). Construcción de la Distribución de pérdidas y el problema de agregación de riesgo operativo bajo modelos LDA: una revisión. Revista Ingenierias Universidad de Medellín, 12(23), 71-82.

Valencia, A. M. (2014). El uso de la distribución g-h en riesgo operativo. Contaduria y Administración, 1(59), 123-148.